Manual Income Verification Services: The Complete Employer Outreach and Documentation Guide

Manual income verification fills the gaps automated data sources miss. This guide explains how employer outreach, document review, and audit-ready documentation work across lending, mortgage, and tenant screening workflows.

Manual Income Verification Services: The Complete Employer Outreach and Documentation Guide

Most income verification files never need a human touch. Automated payroll databases and consumer-permissioned data sources handle the bulk of volume in lending, mortgage, and tenant screening workflows. But when those sources return a "no hit," deliver stale data, or simply do not cover the employer in question, someone has to pick up the phone, send the fax, or draft the email. Manual income verification is that exception-handling layer: a human-powered workflow combining direct employer outreach with document review to close the gaps that automation leaves open.

This guide is written for operations leaders, lenders, property managers, and verification buyers who need to evaluate when manual processes are necessary, what good execution looks like, and how to choose an income verification provider that delivers audit-ready results at scale.

Manual income verification is the process of contacting an employer or income source directly by phone, email, or fax to confirm employment status, income amount, and tenure, then documenting the results in a structured, audit-ready file. It is used when automated payroll databases and digital verification services cannot cover the employer, income type, or documentation scenario. Manual income verification services are most common in mortgage lending, consumer finance, and tenant screening workflows where regulatory or underwriting standards require documented confirmation of income.

What manual income verification actually is

Manual income verification is a structured process where a trained verifier contacts an employer or income source directly, collects or reviews supporting documents, resolves discrepancies, and produces a documented file ready for underwriting, screening, or audit review.

.jpg)

The typical workflow follows a clear sequence. Intake and triage determine which files need manual handling. Outreach to the employer happens by phone, email, or fax, depending on what the employer will accept. The verifier then collects or cross-references documents like paystubs, W-2s, offer letters, or tax records against what the employer confirms verbally or in writing.

Discrepancy resolution is where manual paystub verification and employer outreach income verification earn their keep. When a paystub shows a different employer name than the one listed on an application, or when year-to-date earnings do not align with stated salary, a human verifier can ask follow-up questions, request additional records, and document the outcome. The final deliverable is a verification record with timestamps, contact details, facts confirmed, and any supporting documents attached.

Why manual workflows still exist

Manual income verification persists because automated databases have structural coverage limits. No single payroll aggregator or consumer data source covers every employer, every income type, or every documentation scenario. When a file falls outside automated coverage, the choice is between manual outreach and an incomplete record.

Hard-to-verify employers

Small businesses, franchises, and decentralized employers are common sources of verification friction. A five-person landscaping company is unlikely to participate in a payroll database. A franchise location may route verification requests to a corporate office that takes days to respond, or the franchisee may handle payroll independently.

Some employers respond only to legacy channels. Fax remains the preferred verification method for a meaningful share of small and mid-size employers, particularly in healthcare, construction, and food service. Phone-based verification is sometimes the only option when an employer lacks a dedicated HR function and no one monitors a general email inbox.

Nontraditional income

1099 income verification, gig worker income verification, seasonal employee verification, and multi-job holder verification all create complexity that automated systems handle poorly. A rideshare driver earning income across two platforms and a part-time retail job has no single employer to call. A seasonal construction worker may show strong earnings for eight months and near-zero income for four.

Variable income verification requires more than a single data point. Verifiers may need to collect multiple months of bank statements, review 1099 forms, or confirm employment dates and pay rates with several separate employers. The documentation burden for these cases is higher, and the risk of an incomplete file is greater without manual follow-through.

Incomplete or inconsistent records

Stale paystubs are one of the most common triggers for manual review. Fannie Mae guidance, for instance, requires that the most recent paystub be dated no earlier than 30 days prior to the initial loan application date and include year-to-date earnings. When an applicant provides a paystub that is six weeks old or missing YTD figures, someone has to obtain a current one or verify the gap through employer outreach. Fannie Mae Standards for Employment and Income Documentation

Mismatched employer names, conflicting pay rates between documents, and missing records for recent job changes all require human judgment. Automated systems flag these issues but cannot resolve them.

High-stakes timing windows

Mortgage closings create tight verification windows. Fannie Mae requires verbal verification of employment within 10 business days prior to the note date for employment income, and within 120 calendar days prior to the note date for self-employment income. Fannie Mae Verbal Verification of Employment

When a closing is scheduled for next Tuesday and the automated VOE comes back empty, a manual outreach team that can reach the employer by phone the same day becomes operationally necessary. Lease approvals, urgent lending decisions, and overflow spikes during peak seasons create similar pressure. The ability to execute fast, documented employer outreach income verification on a compressed timeline separates reliable manual verification from a bottleneck.

Common use cases by industry

Manual income verification shows up wherever automated coverage falls short, but the triggers and documentation standards vary by industry.

Lending and consumer finance

Consumer lenders encounter manual verification needs most often with borrowers who have variable income, recent job changes, or employers outside major payroll databases. CFPB-linked mortgage rules under Regulation Z reinforce that creditors rely on reasonably reliable third-party records to assess income and employment, and that a creditor may treat employment as current if the employer verifies it and does not indicate otherwise. CFPB Appendix Q to Regulation Z

For lending income verification operations, manual verification is an exception-handling workflow. A borrower who earns commission income across two roles, or who recently transitioned from 1099 to W-2 employment, may need direct employer confirmation to satisfy underwriting conditions.

Mortgage

Mortgage is the industry where manual income verification standards are most explicitly defined. Fannie Mae maintains dedicated guidance for both verbal verification of employment and employment/income documentation. These are not legacy requirements scheduled for retirement; they are active, embedded standards that lenders follow near closing and for exception cases.

A common mortgage income verification scenario: the borrower's employer is a small medical practice with four employees. The practice does not participate in any automated verification database. The lender's operations team (or outsourced provider) contacts the practice directly by phone, confirms the borrower's position, hire date, and salary, and documents the call with a timestamp, the name and title of the person who confirmed the information, and the specific facts verified.

Tenant screening and property management

Property managers need defensible income records for rental applicants, particularly when the applicant's income is irregular, self-reported, or difficult to confirm through standard channels. A freelance graphic designer applying for an apartment may provide bank statements and 1099 forms, but the property manager still needs to verify that the income is ongoing and sufficient.

HUD-related housing administration materials outline a useful documentation standard for oral verification: record the date and time of the conversation, the name and title of the third party, and the facts verified. HUD Handbook 4350.3 While private-market landlords are not bound by HUD handbook requirements, the operational principle transfers directly. Tenant screening income verification files built on structured documentation protect the property manager in disputes, fair housing inquiries, and internal audits.

Broader verification operations

Some organizations outsource manual verification to handle overflow volume without adding headcount. During peak lending seasons or lease-up periods, internal teams may not have the capacity to work every exception file. A manual income verification provider that operates as an extension of internal operations, using the buyer's templates, escalation rules, and documentation standards, absorbs the surge without degrading file quality.

An outsourced human-powered verification team, like the model Superunit operates, can handle phone, email, and fax outreach at scale while following the buyer's documentation standards. This approach lets an internal team that handles 80% of files through automation route the remaining 20% to a manual verification partner, maintaining turnaround times across the full portfolio.

What a strong manual income verification process looks like

A reliable manual verification workflow has four distinct phases: intake, outreach, escalation, and documentation.

Intake involves receiving the verification request, confirming what needs to be verified (employment status, income amount, tenure, job title), and identifying the employer contact or fallback contact methods. Good intake also includes reviewing any documents the applicant has already provided, since these shape the outreach strategy and surface discrepancies upfront.

Outreach is the core of the process. The verifier contacts the employer by the most effective channel available: phone, email, or fax. For employers that do not respond on the first attempt, a structured follow-up cadence with multiple channels increases the probability of completion. A single phone call with no follow-up is not a verification process; it is a checkbox.

Escalation handles files that cannot be completed through standard outreach. The employer may be unresponsive, the applicant's information may be inconsistent, or the verifier may reach a person who cannot confirm the requested details. Escalation paths should include supervisor-level contacts, alternative verification methods (such as document-only verification when verbal confirmation is not possible), and clear rules for when a file is marked incomplete.

Documentation is where the file becomes audit-ready. Every contact attempt, every piece of information confirmed or denied, every supporting document collected, and every discrepancy noted should be captured in a structured format. This is the deliverable that downstream consumers (underwriters, compliance reviewers, property managers) actually rely on.

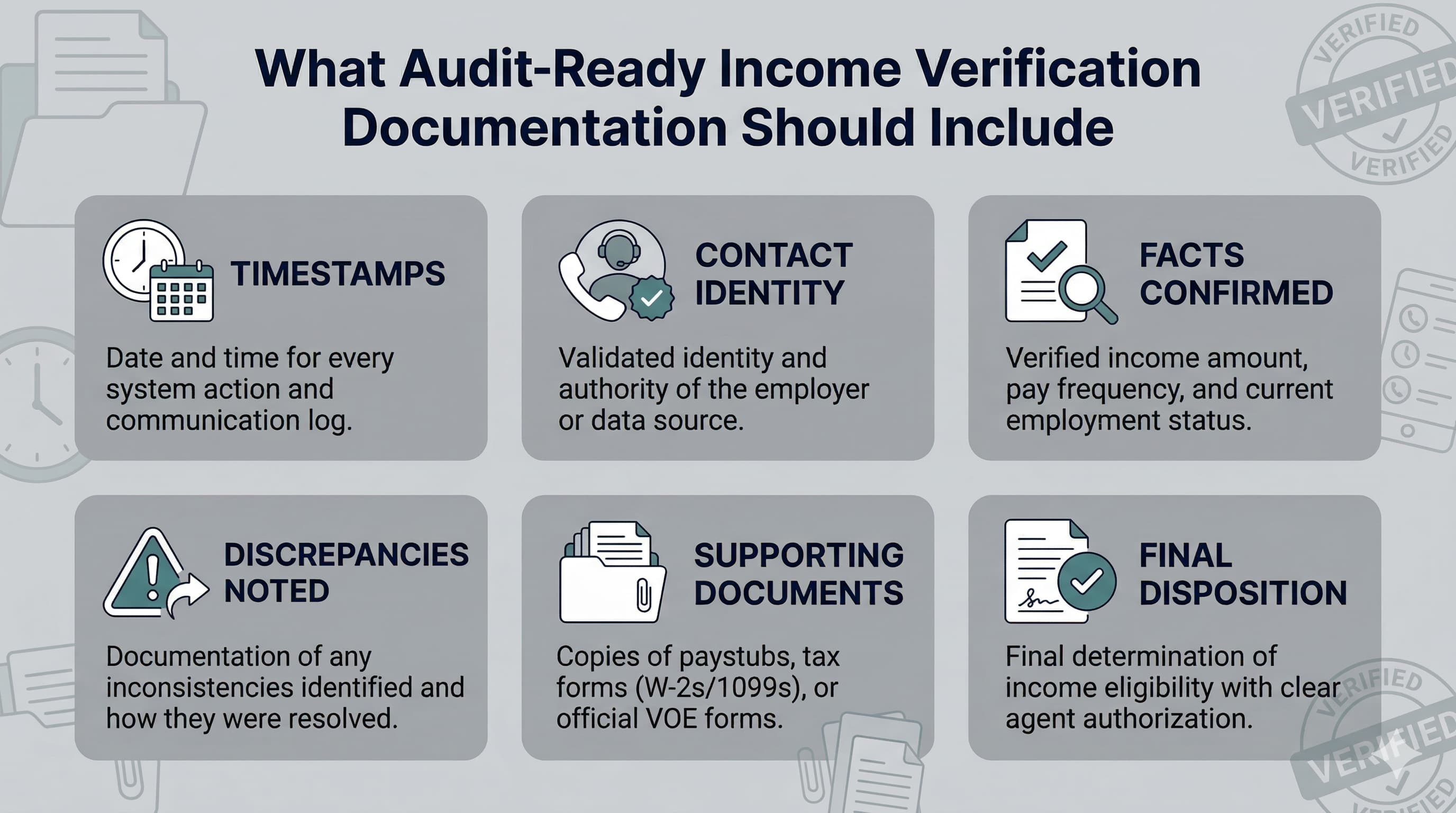

What audit-ready income verification documentation should include

Audit-ready documentation is the primary output of a manual income verification workflow. A file that cannot withstand review by an auditor, examiner, or internal QC team has limited value regardless of how quickly it was completed.

Audit-ready verification record checklist:

- Date and time of each contact attempt and successful contact

- Contact identity: name, title, and phone number or email of the person who provided the information

- Facts confirmed: employment status, hire date, job title, pay rate or salary, pay frequency, year-to-date earnings, and any other data points requested

- Discrepancies identified: any differences between what the applicant provided and what the employer confirmed, along with resolution steps taken

- Supporting documents: copies of paystubs, W-2s, offer letters, or other records collected during the process, with notes on how they were obtained

- Final disposition: whether the verification was completed, partially completed, or unable to be completed, with an explanation

HUD housing verification standards are instructive here. When oral verification is used, documentation should capture the date, time, third-party identity, and specific facts confirmed. PHFA Third-Party Verifications Even outside regulated housing contexts, following a similar standard protects the buyer's file integrity.

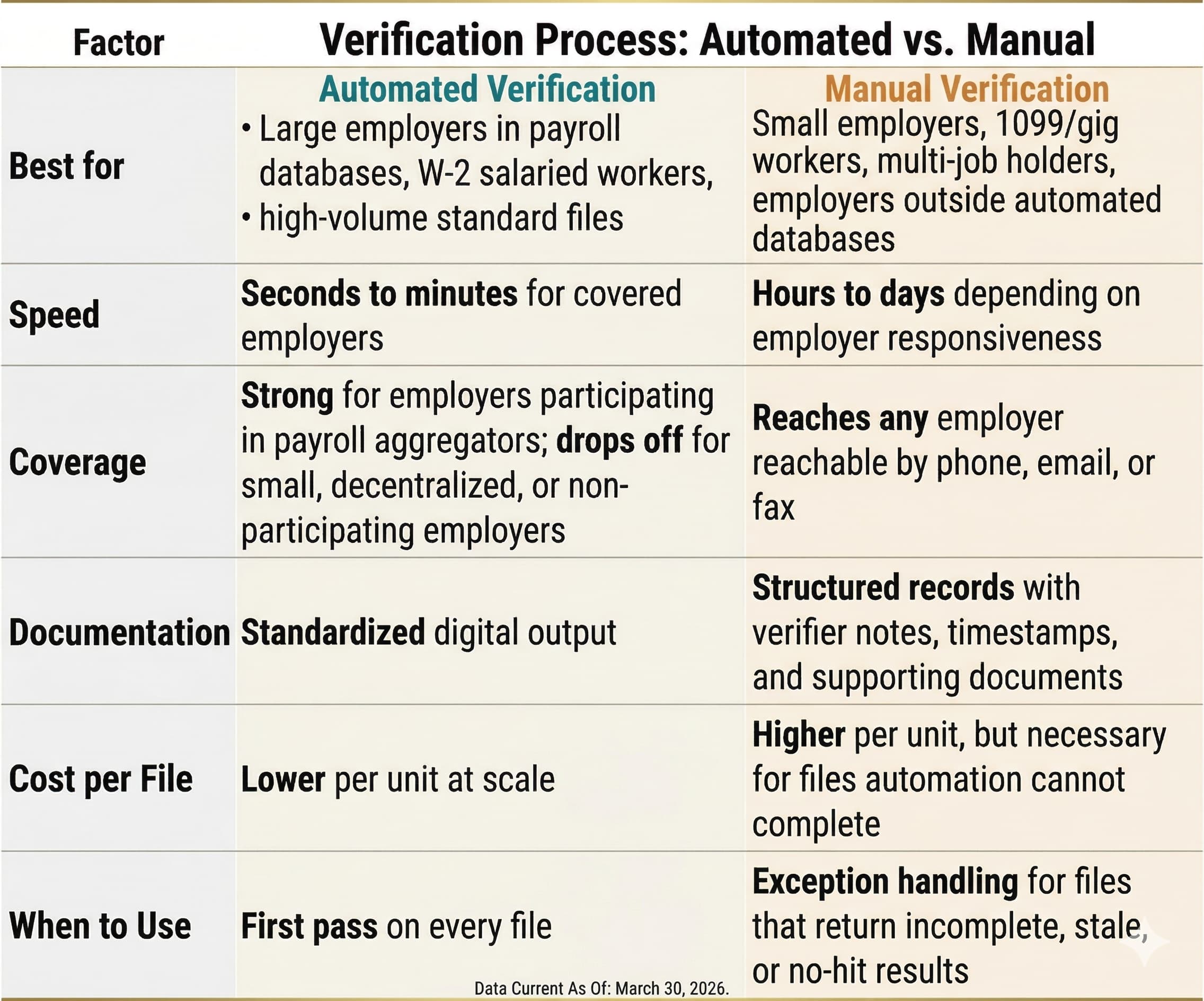

Manual vs. automated income verification: a buyer's decision framework

Manual verification is not a competitor to automated income verification. It is the structured fallback that makes automated workflows viable at scale.

The strongest operational model uses automation as the first pass and manual income verification services as the structured exception-handling layer. Automated sources handle the high-coverage, low-friction files. Manual outreach handles the rest: small employers, nontraditional income, stale documents, unresponsive databases, and tight timing windows.

Buyers evaluating income verification providers should think about integration with their automated workflow, not replacement of it. The right provider, whether an outsourced team like Superunit or an internal manual verification function, accepts the files that automation cannot complete and returns them with the same (or better) documentation quality that the automated source would have provided.

How to evaluate manual income verification providers

Choosing a manual income verification provider is an operational decision, not a procurement formality. The provider becomes part of your verification workflow, and their output directly affects file quality, turnaround, and audit outcomes.

Coverage

Coverage is the most fundamental evaluation criterion. Can the provider reach small employers with no HR department? Can they handle decentralized organizations where payroll is managed at the franchise or location level? Can they verify nontraditional income for 1099 workers, gig economy participants, or applicants with multiple part-time jobs?

Ask how they handle employers that do not respond to initial outreach. A provider with a single-channel approach (phone only, for example) will struggle with employers that prefer fax or email. Multi-channel outreach capability, including phone, email, and fax, is a baseline requirement for broad coverage.

Turnaround time

Standard turnaround, rush SLAs, and escalation speed all matter. A provider that delivers most files in 24 to 48 hours but cannot handle same-day requests during a closing crunch creates risk for mortgage and lending operations.

Ask about overflow handling capacity. If your volume doubles during a peak period, can they absorb the increase without extending turnaround times? Scalable turnaround is more valuable than a fast average that breaks under load.

Documentation quality

Request sample verification records before signing a contract. Look for structured fields, consistent formatting, and the specific elements described in the audit-ready documentation checklist above. If the provider's sample output is a paragraph of free-text notes with no timestamps or contact details, the file will not hold up under scrutiny.

Consistency matters as much as completeness. Every file should follow the same documentation template, regardless of which verifier handled it.

Operational scalability

Evaluate whether the provider can function as an extension of your internal operations, not just a vendor you send files to. Can they work within your systems, follow your escalation rules, and adapt to your documentation templates?

Providers that require you to conform entirely to their workflow may work for small, occasional volumes. For operations teams routing hundreds or thousands of exception files per month, the provider needs to fit into your process. Superunit's model, for example, is built around adapting to the buyer's templates, escalation rules, and quality standards rather than forcing a one-size-fits-all workflow.

Workflow flexibility

Different use cases require different workflows. A mortgage pre-close verbal VOE has different requirements than a tenant screening income check. A lending exception file for a self-employed borrower may require document collection and analysis, not just a phone call.

Check whether the provider supports use-case-specific process variations. Can they handle verbal-only verification, document-only verification, and combined workflows? Do they support phone, email, and fax outreach based on what the employer requires?

Questions buyers should ask before choosing a provider

Practical evaluation questions can reveal more than a capabilities deck. Consider asking:

- What happens when an employer does not respond after three contact attempts? Walk me through the escalation path.

- How do you document a verification where the employer provides partial information?

- Can you show me three sample verification records for different income types (salaried, hourly, 1099)?

- What is your completion rate for employers with fewer than 50 employees?

- If I need 200 verifications completed this week and 50 next week, how do you handle the volume swing?

- Can your verifiers follow our documentation template, or do we use yours?

- How do you handle a file where the applicant's documents conflict with what the employer confirms?

The answers to these questions expose how the provider handles the hard cases, not just the routine ones.

Common mistakes in manual income verification programs

Vague notes instead of structured records. A verification note that reads "Called employer, confirmed employment" tells an auditor almost nothing. Without a timestamp, contact name, and specific facts confirmed, the record is functionally useless for compliance or dispute resolution.

Single-channel outreach. Relying exclusively on phone calls means losing every employer that prefers fax or email. A surprising number of small employers, medical offices, and government agencies still require fax for employment verification. Providers that cannot adapt their outreach channel to the employer's preference will have lower completion rates.

Poor triage and routing. Not every file needs manual verification, and not every manual file needs the same level of effort. Sending a straightforward salaried W-2 employee through a full manual workflow wastes time. Failing to flag a complex multi-job 1099 file for senior review wastes quality. Good triage separates quick confirmations from files that need deep investigation.

Measuring speed without measuring quality. A fast turnaround on a poorly documented file creates more risk than a slower turnaround on a complete one. Buyers should track documentation completeness and audit pass rates alongside turnaround time.

Bottom line

Manual income verification exists because employer databases have coverage limits, income comes in dozens of forms, and regulated workflows still require documented human confirmation in specific scenarios. Fannie Mae verbal VOE requirements, CFPB documentation expectations, and HUD verification standards all reflect the same operational reality: someone has to confirm the information, document the confirmation, and build a file that holds up under review.

When evaluating manual income verification services, focus on the fundamentals. Can they reach the employers your automated sources miss? Can they handle 1099 income verification, gig worker income verification, and complex multi-job files? Do they produce structured, audit-ready documentation on every file? Can they scale with your volume and adapt to your workflow? A provider that combines outreach discipline, documentation rigor, and flexible execution (the model Superunit was built around) is the one that keeps your exception files from becoming your weakest link.

Frequently asked questions

What is manual income verification?Manual income verification is the process of contacting an employer or income source directly by phone, email, or fax to confirm a person's employment status, income, and tenure. A trained verifier collects or reviews supporting documents, resolves discrepancies, and produces a structured, audit-ready record. It is used when automated payroll databases and digital verification tools cannot cover the employer or income type.

When is manual income verification used instead of automated verification?Manual verification is used when automated sources return a "no hit," deliver stale data, or do not cover the employer. Common triggers include small employers not participating in payroll databases, 1099 and gig worker income, recent job changes, stale paystubs, and tight closing or approval timelines where same-day employer outreach is required.

How does manual income verification differ from automated verification?Automated verification pulls data from payroll aggregators and consumer-permissioned databases in seconds. Manual verification involves a human verifier contacting the employer directly and documenting the results. Automated systems work well for large employers in participating databases. Manual verification covers the rest: small businesses, franchises, nontraditional income, and any employer outside automated coverage.

What documentation is required for manual income verification?An audit-ready manual verification file should include the date and time of each contact attempt, the name and title of the person who confirmed the information, the specific facts verified (employment status, hire date, pay rate, pay frequency, year-to-date earnings), any discrepancies found and how they were resolved, copies of supporting documents, and the final disposition of the verification.

How should buyers evaluate manual income verification providers?Evaluate providers on five criteria: coverage (can they reach small, decentralized, and nontraditional employers), turnaround time (including rush and same-day SLAs), documentation quality (structured records, not free-text notes), operational scalability (ability to absorb volume swings), and workflow flexibility (support for phone, email, fax, and use-case-specific processes). Ask for sample verification records and completion rates for small employers before signing a contract.

What types of income are hardest to verify manually?1099 contractor income, gig worker income, seasonal employment, tipped wages, and multi-job holders are among the hardest to verify. These cases often require outreach to multiple employers or income sources, collection of several months of bank statements or 1099 forms, and more documentation than a standard salaried W-2 verification.

Ready to get started?

Major CRAs trust us to handle the verifications no one enjoys — faster, cheaper, and fully documented. See how!