Mortgage Employment Verification Providers: How to Compare VOE and VOI Options

Neutral comparison of mortgage employment verification providers across payroll connectivity, database, manual outreach, and orchestration models, with guidance on evaluating VOE and VOI vendors by completion rate, turnaround time, compliance, auditability, and LOS integration.

Mortgage Employment Verification Providers: How to Compare VOE and VOI Options

A late verification of employment can stall a closing faster than almost any other single bottleneck. When a VOE or VOI comes back incomplete, in the wrong format, or outside an agency timing window, the delay hits underwriting, lock extensions, and borrower trust. The mortgage VOE vendor you choose determines how often that happens and how much your team scrambles to fix it.

The market for mortgage income verification providers is fragmented. Argyle, in its comparison of verification providers, frames the landscape as a "patchwork" problem where lenders rely on multiple vendors across VOI, VOE, VOA, and document workflows. No single provider covers every scenario, but a clear framework makes the comparison manageable. Lenders evaluating their options will encounter payroll connectivity providers like Argyle and Truv, database providers like Equifax's The Work Number, orchestration platforms like Truework and Informative Research, and completion-focused verification vendors like Superunit that prioritize manual outreach, reverification support, and audit-ready documentation.

This guide compares the four main provider models, then compares specific brands. It is written for mortgage operations leaders, underwriting teams, and verification managers evaluating which approach fits their borrower mix and compliance requirements.

Key Takeaways

- Four provider models dominate mortgage employment verification: payroll connectivity, database-based (e.g., The Work Number), manual outreach, and multi-method orchestration.

- No single model covers every borrower. Lenders with variable pipelines typically need either orchestration or a deliberate multi-vendor strategy.

- Completion rate matters more than speed on the initial pull. A fast failure that triggers a second attempt is slower and more expensive than a slightly longer pull that completes the first time.

- Agency timing requirements from Fannie Mae and Freddie Mac make reverification support a hard requirement, not a nice-to-have.

- Evaluate providers on total cost per closed loan, not per-order price, because fallback attempts and manual completion change the math.

Which provider model fits which lender?

- Lender situation: Digital-first lender with strong borrower engagement and high consent completion | Best-fit model: Payroll connectivity (e.g., Argyle, Truv, Plaid)

- Lender situation: High volume with most borrowers at large or mid-size employers | Best-fit model: Database verification (e.g., Equifax's The Work Number)

- Lender situation: Serving many small employers, self-employed, or gig-adjacent W-2 borrowers, and needing reliable reverification and file-ready documentation | Best-fit model: Manual outreach or a completion-focused provider (e.g., Superunit)

- Lender situation: Mixed borrower population, variable employer sizes, need for one ordering workflow | Best-fit model: Multi-method orchestration (e.g., Truework, Informative Research)

Why mortgage verification provider choice matters

Agency timing requirements create real pressure. Fannie Mae's Selling Guide requires that a verbal verification of employment be obtained within 10 business days prior to the note date for employment income, and within 120 calendar days for self-employment income. If your verification provider cannot support pre-close reverification within those windows, your team absorbs the gap with phone calls.

Fragmented vendor stacks add handoffs. When one provider handles instant database pulls and another handles manual outreach, your operations team manages two ordering systems, two sets of reporting, and two escalation paths. Poor provider fit increases fallout, manual touches, and the likelihood of a file reaching the closing table with incomplete documentation.

How mortgage VOE and VOI work

VOE confirms that a borrower is currently employed. VOI validates the income used for qualification, typically through pay statements, W-2s, or payroll records. Lenders may use verbal checks, written documentation, or third-party verification reports depending on the loan program.

Truework breaks the landscape into two broad categories: manual verification and third-party VOE providers. Manual verification means contacting employers directly by phone, fax, or email. Third-party providers supply verification reports through payroll data access, employer record databases, or orchestrated multi-method platforms.

Common verification methods

Employer outreach is the oldest method. A processor or vendor calls or emails the employer's HR department, requests confirmation of employment dates and income, and documents the response. It works everywhere but scales poorly.

Payroll-connected verification pulls data directly from payroll systems with borrower permission. The data is current-state and often includes detailed income breakdowns, making it strong for both VOE and VOI.

Database-based verification returns records from large employer databases. When a record exists, the result is nearly instant. When it does not, lenders need a fallback path, which is why many teams evaluating The Work Number alternatives look at providers with built-in manual completion.

Waterfall routing combines multiple methods in sequence. A verification order starts with the fastest or cheapest path and falls through to alternatives when the primary method returns no result.

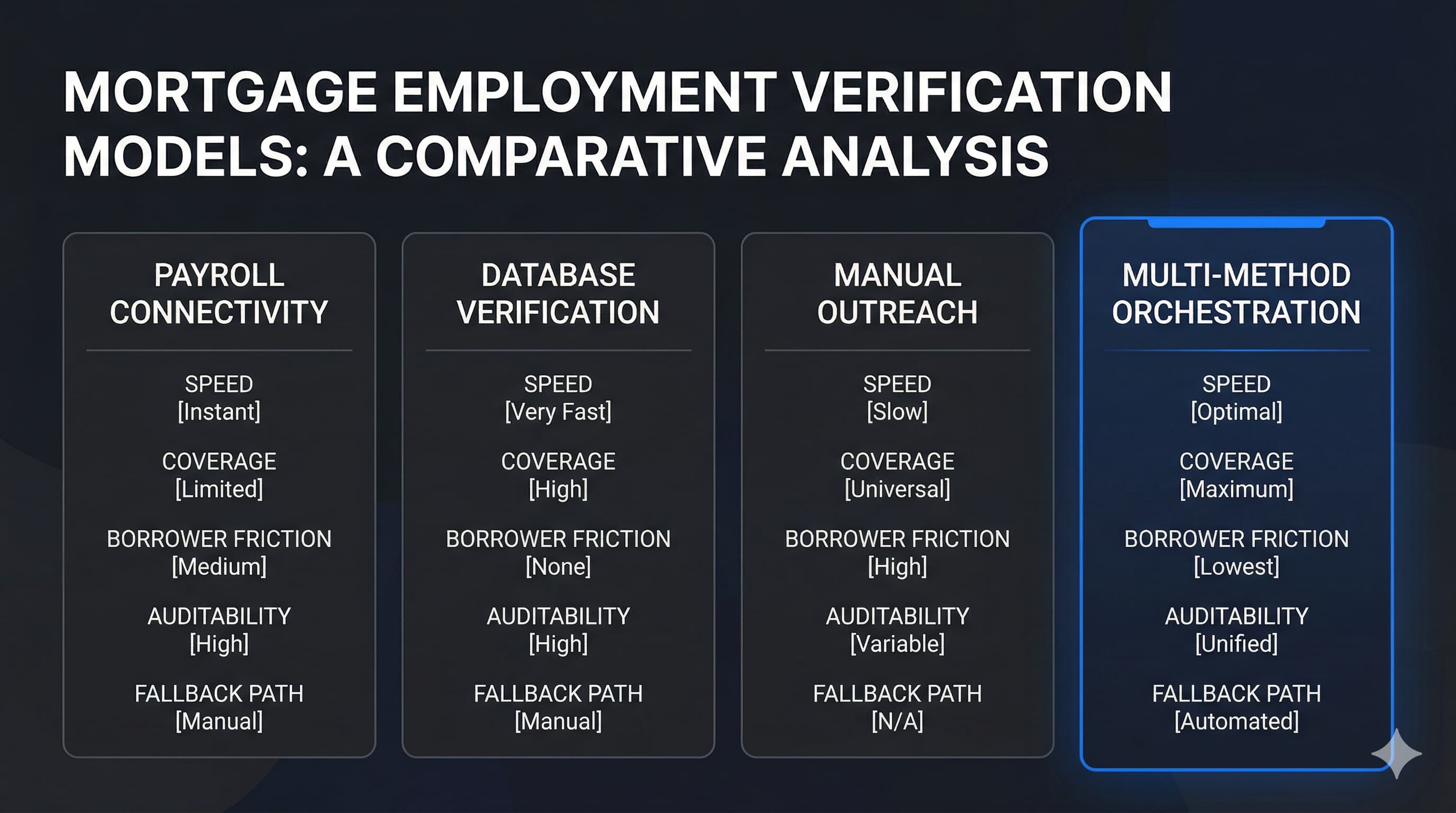

The four main provider models

Payroll connectivity providers

Payroll connectivity providers pull employment and income data directly from a borrower's payroll system. The borrower authenticates through a consent flow, and the provider returns pay history, employment dates, and income details from the source of record.

Best for: Digital-first lenders with strong borrower engagement and a need for current-state payroll data.

Pros:

- Direct-source payroll data reduces reliance on static records and gives underwriters current pay period detail

- Faster turnaround on connected pulls because data retrieval does not depend on employer responsiveness

- Lower manual follow-up when connection rates are high, since data arrives without processor intervention

Cons:

- Coverage depends on borrower action. If a borrower does not complete the credential step, the pull fails and you need a fallback.

- Payroll system compatibility varies. Not every employer's payroll platform is supported, which creates gaps for certain borrower segments.

Database-based providers

Database verification providers maintain or access large repositories of employer-reported employment and income records. The most well-known example is Equifax's The Work Number, which covers a substantial share of the U.S. workforce.

Best for: Lenders who need instant results for a large share of their pipeline and already have processes built around database pulls.

Pros:

- Instant results when records exist make database pulls strong for preapproval screening and fast conditional approvals

- Broad employer record access across large and mid-size employers that contribute payroll data

- Lower borrower friction because the borrower does not need to authenticate or upload anything at order time

Cons:

- Coverage gaps require fallback paths. Equifax's own developer documentation states that when VOE/I is not instantly available through The Work Number, users can "seamlessly waterfall to manual verification solutions." That acknowledgment tells you gaps are expected.

- Data can be static. Records may reflect the most recent payroll contribution rather than true current-state employment, which matters for pre-close reverification.

Manual outreach providers

Manual outreach providers contact employers directly to complete verification requests. This is the fallback path that nearly every lender eventually needs, whether handled in-house or through a vendor.

Best for: Completing verifications for borrowers who fall outside instant coverage, particularly those with smaller employers or non-standard employment.

Pros:

- Strong for edge cases where instant data sources have no record, such as small businesses, new employers, or gig-adjacent W-2 work

- Detailed documentation output because the verification is completed through direct employer contact, which often produces the kind of written confirmation Freddie Mac requires in the mortgage file

- No borrower credential requirement since the outreach goes to the employer, not the borrower

Cons:

- Turnaround time varies widely. Employer responsiveness is the bottleneck, and some HR departments take days or weeks to reply.

- Harder to scale during volume spikes because each order requires human follow-up, queue management, and sometimes multiple contact attempts.

Orchestrated multi-method platforms

Orchestration platforms route each verification order to the method most likely to succeed based on employer data, borrower profile, or hit-rate history. Informative Research, for example, describes its verification platform as aligning each order with the provider most likely to succeed and tracking hit rates, turnaround times, and usage trends across methods.

Best for: Lenders with a variable borrower mix who want one ordering interface, consolidated reporting, and better completion logic across verification methods.

Pros:

- Intelligent method selection improves completion. Rather than starting every order with the same approach, orders flow to the path with the highest probability of success for that specific case.

- Consolidated reporting across methods gives operations managers visibility into hit rates, turnaround time distributions, and cost per completed verification, not just per order.

- Single ordering interface reduces the swivel-chair problem where processors must decide which vendor to try first, then manually re-order through a different system when the first attempt fails.

- Fallback logic is built in. When an instant pull fails, the order routes to manual outreach or an alternative provider without requiring a new submission.

Cons:

- Method selection quality varies by provider. An orchestration layer is only as good as its underlying data sources and decision logic. Ask how the platform selects methods and whether selection adapts over time.

- Transparency can be uneven. Some orchestration platforms abstract the underlying provider, which can make it harder to audit exactly how a verification was completed unless the reporting is detailed.

Truework takes a similar approach, promoting multi-method orchestration with intelligent verification method selection and performance tracking across methods. The common thread is that orchestration tries to solve the coverage and speed problem simultaneously rather than forcing lenders to pick one.

Brand comparison: Argyle, Truework, Equifax, Superunit, and Informative Research

The table below compares five mortgage VOE providers by model, noted strengths, tradeoffs, and where each tends to be the strongest choice. Claims are based on vendor documentation and public product pages, not independent benchmarks.

- Provider: Argyle | Model: Payroll connectivity | Strengths: Current-state payroll data; no reliance on employer-contributed databases; broad payroll integrations | Tradeoffs: Completion depends on borrower consent and payroll platform support; no built-in manual fallback | Best-fit use case: Digital-first lenders with high borrower engagement who want a The Work Number alternative for direct-source data

- Provider: Truework | Model: Multi-method orchestration | Strengths: Routes orders across instant and manual methods; performance tracking and transparency reporting; supports both VOE and VOI | Tradeoffs: Orchestration quality depends on underlying provider network; less control over which specific source completes a given order | Best-fit use case: Lenders with mixed borrower populations who want a single mortgage income verification provider across methods

- Provider: Equifax / The Work Number | Model: Database verification | Strengths: Largest U.S. employer-contributed database; near-instant results when records exist; low borrower friction | Tradeoffs: Coverage gaps for smaller employers require manual fallback; data may be static rather than current-state; pricing can be higher per pull | Best-fit use case: High-volume lenders whose borrowers are concentrated at large and mid-size employers

- Provider: Superunit | Model: Manual outreach and completion-focused verification | Strengths: Strong completion rates on employer outreach; reverification workflow support; audit-ready documentation designed for agency file requirements | Tradeoffs: Turnaround depends on employer responsiveness; less suited for lenders whose primary need is instant database pulls | Best-fit use case: Lenders prioritizing first-attempt completion, pre-close reverification reliability, and file-ready documentation across smaller or harder-to-reach employers

- Provider: Informative Research | Model: Multi-method orchestration | Strengths: Provider-agnostic order routing; hit-rate and turnaround tracking; consolidated reporting across methods | Tradeoffs: Routing logic is a black box unless reporting is granular; lender has less direct vendor control | Best-fit use case: Operations teams focused on cost-per-completed-verification and wanting one platform across all methods

Argyle

Argyle built its product around direct payroll connectivity and explicitly compares its approach against The Work Number, Experian Verify, AccountChek, Plaid, and Truv. The company's core argument is that lenders end up managing a patchwork of vendors across VOI, VOE, VOA, and document upload steps, and that direct payroll access consolidates those needs. Where Argyle is strongest: borrowers whose payroll platforms are connected and who complete the consent step. Where it is weakest: borrowers at unsupported employers or those who abandon the credentialing process.

Truework

Truework draws a clear line between manual verification and third-party VOE providers, then argues that orchestration across both is the better path. Orders route to the best-fit verification method rather than defaulting to one source, and Truework tracks how each order was completed. For lenders who want performance data broken down by method, employer type, and turnaround, Truework's reporting emphasis is a differentiator. The tradeoff: lenders cede some control over which specific vendor completes a given verification.

Equifax and The Work Number

Equifax operates the largest employer-contributed database for employment and income verification in the U.S. When a record exists in The Work Number, the result is nearly instant and requires no borrower action. Equifax's developer documentation acknowledges that instant data is not always available and supports waterfall to manual verification, a frank admission that even the broadest database has coverage limits. Lenders evaluating The Work Number alternatives typically cite coverage gaps for smaller employers and per-pull pricing as their primary concerns.

Superunit

Superunit approaches mortgage employment verification with a focus on completion and documentation quality rather than instant data retrieval. Where payroll connectivity and database providers depend on system access or employer-contributed records, Superunit's strength is in direct employer outreach workflows designed to complete verifications that other methods miss, particularly for smaller employers, newer businesses, and cases where database records do not exist.

For lenders whose pipelines include a meaningful share of borrowers outside the reach of instant verification, Superunit's value is in reducing the volume of orders that require processor intervention or a second attempt through a different vendor. Reverification support is a core part of the workflow, which matters given the Fannie Mae 10-business-day pre-note window and Freddie Mac's documentation requirements. Superunit's verification outputs are structured for audit readiness, producing file-ready documentation rather than status-only confirmations.

The tradeoff is speed on the initial pull. Superunit is not designed to compete with database or payroll-connected providers on instant turnaround for borrowers who are already covered by those sources. Its fit is strongest when completion reliability, reverification, and documentation quality carry more weight than sub-second response times.

Informative Research

Informative Research takes a provider-agnostic orchestration approach, routing each verification order to the provider most likely to succeed based on employer data and historical hit rates. Informative Research tracks turnaround times and usage trends, giving operations teams data to adjust provider selection over time. Its value proposition centers on reducing the number of vendor portals a team touches and on lowering cost per completed verification rather than speed alone.

Comparison framework for mortgage teams

1. Coverage and completion rate

Coverage and completion are different measurements. Coverage is the percentage of borrowers a provider can attempt to verify. Completion is the percentage of those attempts that return a usable result.

Ask where instant coverage is strongest. Ask how exceptions are handled when instant data is unavailable. Separate what a provider claims about employer coverage from the actual completion rate your team will experience across your borrower mix, including W-2, 1099, and self-employed cases.

2. Turnaround time

Mortgage verification turnaround time needs to be measured as time-to-usable-report, not time-to-first-attempt. A database pull that returns in seconds is fast, but if 30% of your orders fall to manual outreach that takes three days, your effective turnaround is a blended number.

Ask about SLA consistency, not averages. Ask how the provider handles queue management during volume spikes, and whether pre-close reverification can be triggered automatically or requires a separate order.

3. Compliance and auditability

Freddie Mac requires Form 90 or a similar written document in the mortgage file for verbal VOE. Fannie Mae's 10-business-day window for pre-note reverification means your provider needs to support fast turnaround on repeat checks, not just initial verifications.

CFPB Appendix Q reinforces that income continuity cannot be assumed if a verification indicates employment has been terminated. Verification quality affects ability-to-repay analysis, which means the output must be decision-grade, not a status check. Audit trails should show completion method, data source, and timestamp.

4. Integration and ordering

LOS integration reduces manual ordering steps and improves status visibility. ICE Mortgage Technology's Encompass Partner Connect marketplace categorizes partner connections as automated, one-click, or manual, and promotes automated service ordering and streamlined workflows as explicit benefits. If your team still copies data between systems to order verifications, integration should be near the top of your evaluation criteria.

Reverification should not require rework. The best designs let teams trigger a re-pull from the same interface without re-entering borrower data or switching to a different vendor portal.

5. Borrower experience

Payroll connectivity requires borrower consent and credential entry. If the consent flow is confusing or the credential step fails, completion drops. Manual outreach avoids borrower action entirely but removes borrower control over timing.

Document upload adds another step for the borrower, which can slow completion if borrowers do not respond promptly. Clear fallback paths reduce confusion when one method does not work and the lender needs to try another.

6. Cost structure

Per-order pricing is easy to compare but misleading if completion rates differ. A cheaper pull that fails 40% of the time and triggers a second, paid attempt at manual outreach is more expensive in total than a slightly pricier pull with higher completion.

Ask about reverification pricing, duplicate-order risk in waterfall scenarios, and whether manual completion is priced separately. Measure total cost per closed loan, not unit price per verification attempt.

Agency and compliance considerations

Fannie Mae

The 10-business-day verbal VOE window before the note date is tight enough that a provider with inconsistent reverification turnaround can jeopardize closing. If your mortgage VOE vendor cannot reliably complete a reverification within that window during volume spikes, your processors will end up making phone calls anyway. Speed on the initial verification means little if reverification support is weak.

Freddie Mac

Freddie Mac's requirement for Form 90 or similar written documentation in the mortgage file means verification outputs must be file-ready. A verbal confirmation with no written record does not satisfy the requirement. Providers that return structured, downloadable reports with employer confirmation details reduce the documentation burden on your team.

CFPB and underwriting quality

CFPB Appendix Q makes clear that income continuity cannot be assumed if employment has terminated. Verification is not a checkbox. The quality of the data returned, including whether it reflects current employment status, directly affects underwriting confidence and ability-to-repay analysis. Providers that return stale or ambiguous results create risk that surfaces in QC and audit, not at order time.

Where each provider model tends to fit best

Payroll connectivity fits best when borrower consent rates are strong, LOS integrations are already in place, and teams want current-state payroll data with fewer manual touches. Digital-first lenders with engaged borrowers tend to see the highest completion rates from payroll-connected pulls.

Database verification fits best when instant availability covers a large share of your borrower pipeline, preapproval speed is a priority, and your existing processes already incorporate database pulls. Manual fallback must be available for the portion of orders that do not return a record.

Manual outreach fits best when borrowers fall outside instant coverage, smaller employers are common in your market, and edge cases require human follow-up. Completion rates can be high, but turnaround time varies, and per-order cost is higher.

Multi-method orchestration fits best when your borrower mix is highly variable, your team wants a single ordering interface, and you need consolidated reporting across methods. Orchestration platforms are strongest when both speed and completion matter and when cost control depends on method selection rather than a single data source.

Questions mortgage teams should ask vendors

- What percentage of orders in our borrower profile complete instantly?

- What triggers manual fallback, and how is the handoff managed?

- How is pre-close reverification handled, and is it automated or manual?

- What does the audit trail include for each completed verification?

- Which LOS and POS systems integrate, and at what automation level?

- How are 1099 and self-employed borrowers supported?

- What is priced separately (reverification, manual completion, failed pulls)?

- How are failed pulls resolved, and who owns the escalation?

Practical comparison matrix

- Evaluation area: Speed | Payroll connectivity: Fast when connected | Database verification: Fast when record exists | Manual outreach: Slower, variable | Multi-method orchestration: Depends on method selected

- Evaluation area: Completion resilience | Payroll connectivity: Coverage-dependent | Database verification: Coverage-dependent | Manual outreach: Strong for exceptions | Multi-method orchestration: Strongest across mixed pipelines

- Evaluation area: Borrower friction | Payroll connectivity: Consent and credentials | Database verification: Lower at order time | Manual outreach: Lower for borrower | Multi-method orchestration: Varies by path

- Evaluation area: Audit trail | Payroll connectivity: Vendor-specific | Database verification: Vendor-specific | Manual outreach: Often detailed | Multi-method orchestration: Often strongest

- Evaluation area: Per-order complexity | Payroll connectivity: Moderate | Database verification: Lower initially | Manual outreach: Higher per order | Multi-method orchestration: Lower if unified

- Evaluation area: Best-fit lender | Payroll connectivity: Digital-first lenders | Database verification: Database-heavy pipelines | Manual outreach: Edge cases, small employers | Multi-method orchestration: Mixed borrower populations

FAQ

What is the difference between mortgage VOE and VOI?

VOE confirms that a borrower is currently employed. VOI validates the income details used for loan qualification, such as salary, hourly rate, overtime, or bonus income. Many mortgage employment verification providers support both, but the data sources and documentation requirements can differ.

Why do lenders use multiple verification methods?

No single method covers every borrower. Instant data sources miss employers that do not contribute records, and payroll connectivity depends on borrower action. Fallback paths, whether manual outreach or alternative databases, improve overall completion rates across a mixed pipeline.

What should matter more: speed or completion?

Both matter, but a fast failure still creates a delay. An instant pull that returns no result and requires a second attempt through a different method is slower in total than a single pull that takes a bit longer but completes. Measuring time-to-usable-report across your full borrower mix gives a more accurate picture than looking at instant-pull speed alone.

Why does LOS integration matter for verification?

Manual ordering through a separate portal adds steps, increases error risk, and makes status tracking harder. Automated service ordering through an LOS marketplace reduces those handoffs and helps teams scale reverification without adding headcount.

Are agency requirements relevant to provider choice?

Yes. Fannie Mae's verbal VOE timing window and Freddie Mac's documentation requirements directly affect which providers can support your process. A provider that delivers fast initial verifications but cannot support timely reverification or file-ready documentation creates a gap your team has to fill manually.

What are common alternatives to The Work Number?

Lenders looking for The Work Number alternatives typically evaluate payroll connectivity providers like Argyle, orchestration platforms like Truework or Informative Research, completion-focused outreach providers like Superunit, or other specialized manual outreach vendors. Each addresses a different gap: payroll connectivity offers current-state data without employer-contributed databases, orchestration platforms combine multiple sources under one order, and manual outreach providers like Superunit cover employers that do not appear in any database while delivering audit-ready documentation and reverification support.

Choosing the right model

The best mortgage employment verification provider is the one that matches your borrower population, compliance needs, and closing timeline. Model matters more than brand reputation. A lender originating primarily through digital channels with engaged borrowers may thrive with payroll connectivity, while a lender serving a diverse geographic market with many small employers may need orchestration or strong manual outreach. Lenders whose primary pain points center on first-attempt completion, pre-close reverification reliability, and file-ready documentation should evaluate providers like Superunit that are built around those priorities, particularly when a significant share of the pipeline falls outside instant database or payroll coverage.

Compare method selection logic, completion rates across your actual borrower profile, reverification support, and total cost per closed loan. Use the comparison matrix and vendor questions above to build a shortlist based on what your pipeline actually looks like, not marketing claims. Compliance, completion, and speed should drive the decision, in roughly that order.

Related reading:

Ready to get started?

Major CRAs trust us to handle the verifications no one enjoys — faster, cheaper, and fully documented. See how!